Year-End Tax Planning Tips for Business Owners

Your year-end tax planning should include a careful assessment of your business's financial health and your individual tax situation. It's not just about how much to contribute but also how these contributions align with your overall financial goals.

Year-end tax planning tip for business owners…

Maximize Retirement Contributions!

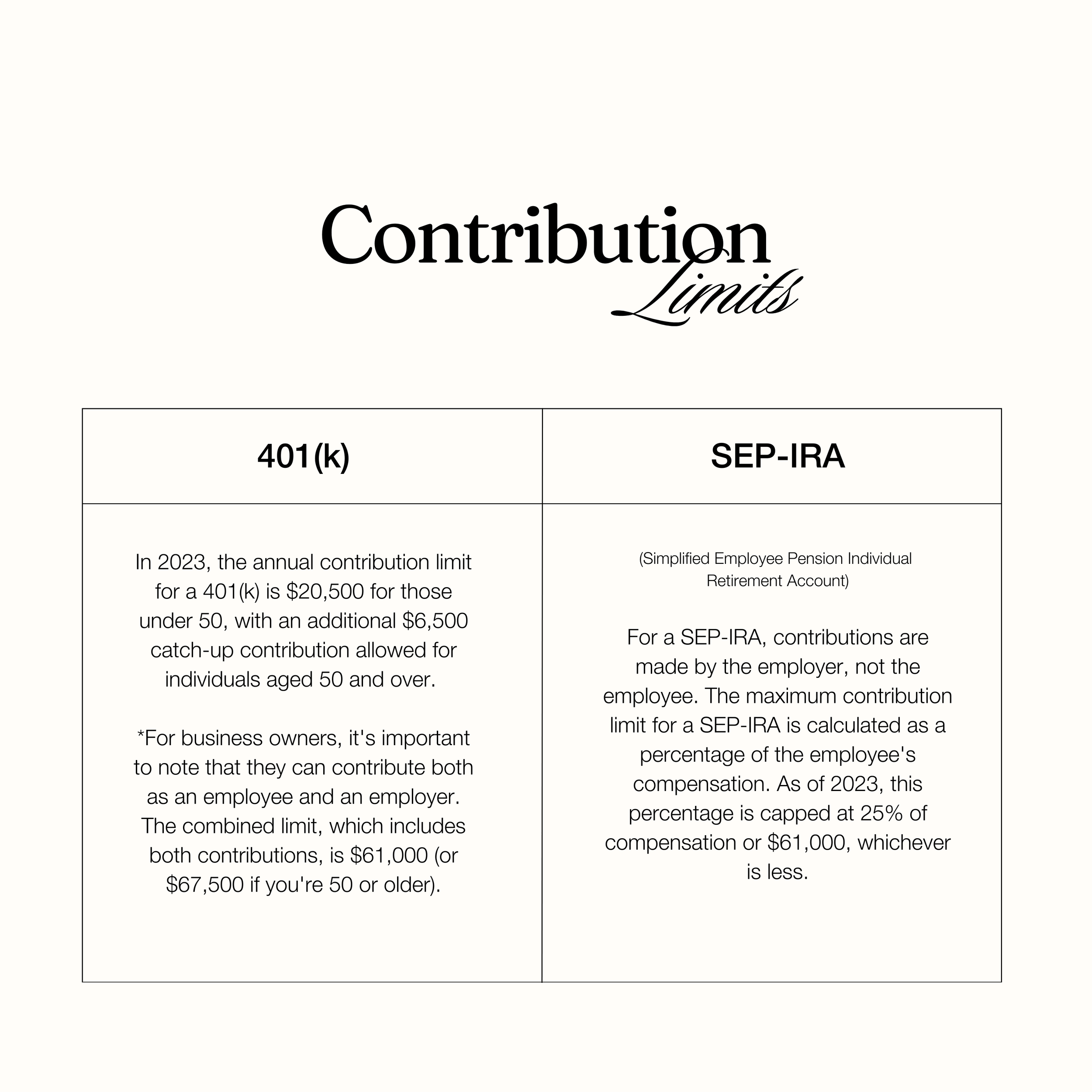

Make sure you're contributing the maximum allowed to your tax-advantaged retirement accounts. This includes a 401(k) or a SEP-IRA, depending on your business structure. Not only do these contributions secure your financial future, but they also reduce your current taxable income.

4 Benefits of Maximizing Contributions

Tax Deferral: Contributions to a 401(k) or SEP-IRA reduce your taxable income for the year in which they are made.

Wealth Accumulation: Contributions to your retirement accounts provide the capital needed for investments that have the potential to grow over time, compounding your wealth and increasing your retirement nest egg.

Asset Protection: Retirement accounts often come with some level of asset protection in case of legal judgments or bankruptcy.

Retirement Security: Maximizing your retirement contributions enhances your financial security in retirement.

Remember that while these contributions provide immediate tax benefits, they are intended for retirement, and early withdrawals may incur penalties and taxes. Therefore, it's essential to work with a financial advisor to navigate the options and strategies for your retirement contributions.

Evaluate Your Business Expenses

A meticulous review of business expenses is a critical component of year-end tax planning. Consider making necessary purchases before the year concludes to optimize tax deductions for the current year. This strategic move not only minimizes tax liability but also positions the business for a financially sound start in the upcoming year.

The timing of these expenditures is key. By strategically planning purchases before the year-end, businesses can capitalize on immediate tax advantages, thus shaping a more favorable financial landscape.

Review Employee Benefits

The year-end provides an opportune moment to assess and potentially adjust employee benefits programs. This includes a review of retirement plans and health insurance offerings. Ensuring these benefits align with both business and employee needs is pivotal for overall financial wellness.

Well-structured and comprehensive employee benefits not only contribute to the financial health of individuals but also enhance overall employee satisfaction and retention.

Explore Tax Credits

Delving into available tax credits specific to your industry or business activities is a nuanced strategy. Identifying and utilizing these credits can significantly impact your overall tax liability.

Understanding the eligibility criteria and optimal utilization of these credits requires a detailed examination. While the process may be intricate, the financial benefits can be substantial.

So, as we head toward the year's end, it's not just about wrapping up another financial chapter. It's about setting the stage for the future. Making smart moves now—whether it's stashing away money for later, optimizing your spending, tuning up employee benefits, or snagging some extra tax perks—can mean a healthier bottom line for your business down the road.

*The opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual.